Featured

Table of Contents

- – Updating the Means Test in Sacramento Californ...

- – Chapter 13 and the Five-Year Plan Extension

- – Medical Financial obligation and the 2026 Exem...

- – Small Company Relief and Subchapter V

- – The Role of Nonprofit Credit Therapy in 2026

- – Real Estate Counseling and HUD Standards

- – Student Loans and the Course to Release

Economic shifts in 2026 have actually led to substantial adjustments in how people and services approach insolvency. High rate of interest and changing work patterns produced a requirement for more versatile legal structures. The 2026 Bankruptcy Code updates focus on broadening access to relief while ensuring that the system stays fair to both financial institutions and debtors. These modifications impact everyone from single-family households in Sacramento California Debt Relief Without Filing Bankruptcy to large-scale business throughout the nation.

Updating the Means Test in Sacramento California Debt Relief Without Filing Bankruptcy

The core of any Chapter 7 filing is the ways test, which figures out if a filer has enough disposable earnings to pay back some of their debts through a Chapter 13 strategy. In 2026, the federal government upgraded the average earnings figures to reflect the sharp rise in housing and energy costs. For residents in Sacramento California Debt Relief Without Filing Bankruptcy, this implies that the threshold for receiving an overall financial obligation discharge has actually increased. Filers whose income falls below the new 2026 state mean are now most likely to qualify for Chapter 7 without the substantial documents previously needed.

The updated code likewise presents a particular allowance for "inflation-impacted expenditures." This allows individuals in various regions to deduct greater expenses for groceries and utilities before the court computes their disposable earnings. These changes acknowledge that a dollar in 2026 does not go as far as it did even a few years back. Increasing interest in Financial Stability has helped clarify the options offered to those dealing with these monetary pressures.

Chapter 13 and the Five-Year Plan Extension

Chapter 13 bankruptcy, frequently called a wage earner's strategy, has seen its own set of 2026 revisions. The main upgrade involves the treatment of home mortgage arrears. Under the new guidelines, house owners in the local vicinity can now extend their repayment prepares to 72 months if they are trying to conserve a primary home from foreclosure. This extra year provides a buffer for families who have actually fallen back due to medical emergency situations or momentary task loss.

Furthermore, the 2026 updates have simplified the "cramdown" process for particular guaranteed financial obligations. In the past, reducing the principal balance on a vehicle loan to the real value of the vehicle was challenging. New 2026 guidelines make this process more available for middle-income filers, offered the loan is at least 2 years of ages. This modification assists numerous individuals keep the transport they require for work while handling a sustainable spending plan.

Medical Financial obligation and the 2026 Exemptions

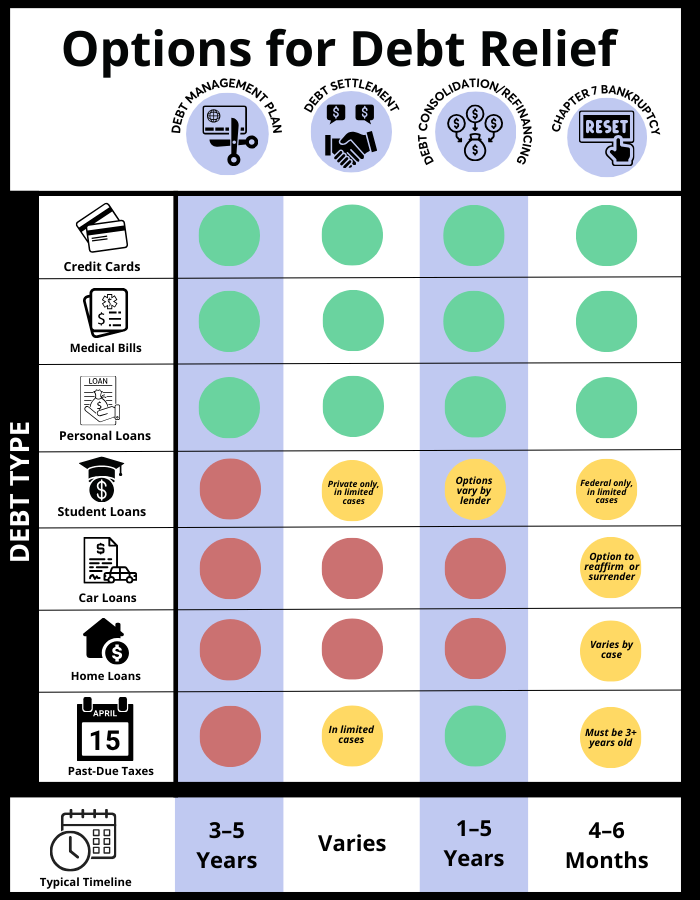

Among the most talked-about modifications in the 2026 Bankruptcy Code is the treatment of medical debt. Recognizing that health-related expenses are the leading reason for insolvency in the United States, the legislature passed the Medical Financial obligation Relief Act of 2026. This law dictates that medical financial obligation is no longer considered in the ways test estimation for Chapter 7 eligibility. Basically, having large medical costs will not prevent somebody from getting approved for insolvency, even if their income is a little above the mean.

Furthermore, 2026 policies prevent medical debt from being reported to credit bureaus once a bankruptcy case is filed. This permits a much faster healing of credit scores for locals in Sacramento California Debt Relief Without Filing Bankruptcy. The objective is to separate inescapable health costs from discretionary spending routines, providing sincere debtors a real clean slate. Strategic Financial Stability Plans offers unique benefits over traditional liquidation for those whose debt is mostly tied to healthcare facility stays or long-lasting care.

Small Company Relief and Subchapter V

Little business owners in the surrounding region have benefited from the permanent extension of the Subchapter V debt limits. At first a short-term step, the 2026 updates have actually set the debt ceiling for small company reorganization at $7.5 million forever. This allows entrepreneurs to keep their doors open while restructuring their commitments without the enormous administrative expenses of a standard Chapter 11 filing.

The 2026 version of Subchapter V likewise consists of a new "debtor-in-possession" security that streamlines the interaction in between service financial obligation and individual liability. For many entrepreneur in Sacramento California Debt Relief Without Filing Bankruptcy, their personal properties are frequently connected to their business loans. The upgraded code supplies a clearer path to protect individual homes and pension during a service restructuring, provided the owner follows a court-approved therapy program.

The Role of Nonprofit Credit Therapy in 2026

Before any individual can submit for personal bankruptcy in 2026, they should complete a pre-filing credit therapy session with a DOJ-approved agency. These companies, often operating as 501(c)(3) nonprofits, serve a crucial function by examining a person's entire monetary photo. In 2026, these sessions have actually ended up being more thorough, integrating digital tools that help citizens in Sacramento California Debt Relief Without Filing Bankruptcy see precisely how an insolvency filing will impact their long-term objectives.

These nonprofit companies do not simply focus on bankruptcy. They likewise use debt management programs (DMP) as an option to legal filings. A DMP consolidates numerous unsecured debts into one month-to-month payment, often with lower rates of interest negotiated straight with creditors. For lots of in the local area, this provides a method to pay back what they owe without the long-lasting impact of an insolvency on their credit report. Those looking for Financial Stability in Sacramento will discover that 2026 guidelines prefer earlier intervention through these nonprofit channels.

Real Estate Counseling and HUD Standards

For those fretted about losing their homes, 2026 has brought a tighter combination between personal bankruptcy courts and HUD-approved housing counseling. If a filer in Sacramento California Debt Relief Without Filing Bankruptcy points out a threat of foreclosure, the court now regularly mandates a session with a real estate therapist. These professionals try to find loan adjustments, partial claims, or other loss mitigation choices that might exist beyond the insolvency process.

This holistic method guarantees that bankruptcy is the last resort rather than the. In 2026, the success rate for Chapter 13 strategies has actually increased due to the fact that filers are better informed on their real estate rights before they enter the courtroom. Financial literacy programs, typically offered by the very same firms that deal with pre-bankruptcy education, are now a requirement for the last discharge of debt. This ensures that the patterns causing insolvency are dealt with, preventing a cycle of repeat filings.

Student Loans and the Course to Release

The 2026 updates have actually lastly attended to the "undue hardship" requirement for student loans, which was historically hard to meet. While student loans are not immediately discharged, the brand-new 2026 Department of Justice guidelines have actually streamlined the process for the court to recognize when a borrower has no practical opportunity of paying back the financial obligation. This is particularly practical for older citizens in Sacramento California Debt Relief Without Filing Bankruptcy who are entering retirement with considerable education financial obligation.

Under the 2026 guidelines, if a debtor has been in repayment for a minimum of 10 years and their earnings is below a specific level, the bankruptcy court can now purchase a partial discharge or a permanent interest rate freeze. This shift acknowledges that education debt has ended up being a structural part of the economy that needs specific legal treatments. The focus has moved from "can the debtor pay?" to "is it equitable to require them to pay?" due to their total financial health.

Browsing the 2026 insolvency environment needs a clear understanding of these brand-new guidelines. Whether it is the exclusion of medical debt, the extension of payment strategies, or the specialized securities for small businesses in various locations, the goal is clear. The 2026 Bankruptcy Code updates aim to supply a more gentle and efficient course back to financial stability for everyone involved.

{kind=link}

Table of Contents

- – Updating the Means Test in Sacramento Californ...

- – Chapter 13 and the Five-Year Plan Extension

- – Medical Financial obligation and the 2026 Exem...

- – Small Company Relief and Subchapter V

- – The Role of Nonprofit Credit Therapy in 2026

- – Real Estate Counseling and HUD Standards

- – Student Loans and the Course to Release

Latest Posts

Advantages of Professional Credit Counseling in 2026

Top Strategies to Handle Credit Balances

Proven Ways of Clearing Liabilities in 2026

More

Latest Posts

Advantages of Professional Credit Counseling in 2026

Top Strategies to Handle Credit Balances

Proven Ways of Clearing Liabilities in 2026